Last week I took the Eurostar to Paris to attend FlotAuto, a fleet trade show. While there, I had the opportunity to step back, observe, and come back with a better understanding of what it is that fleets are focused on these days (or at least what they are being sold to).

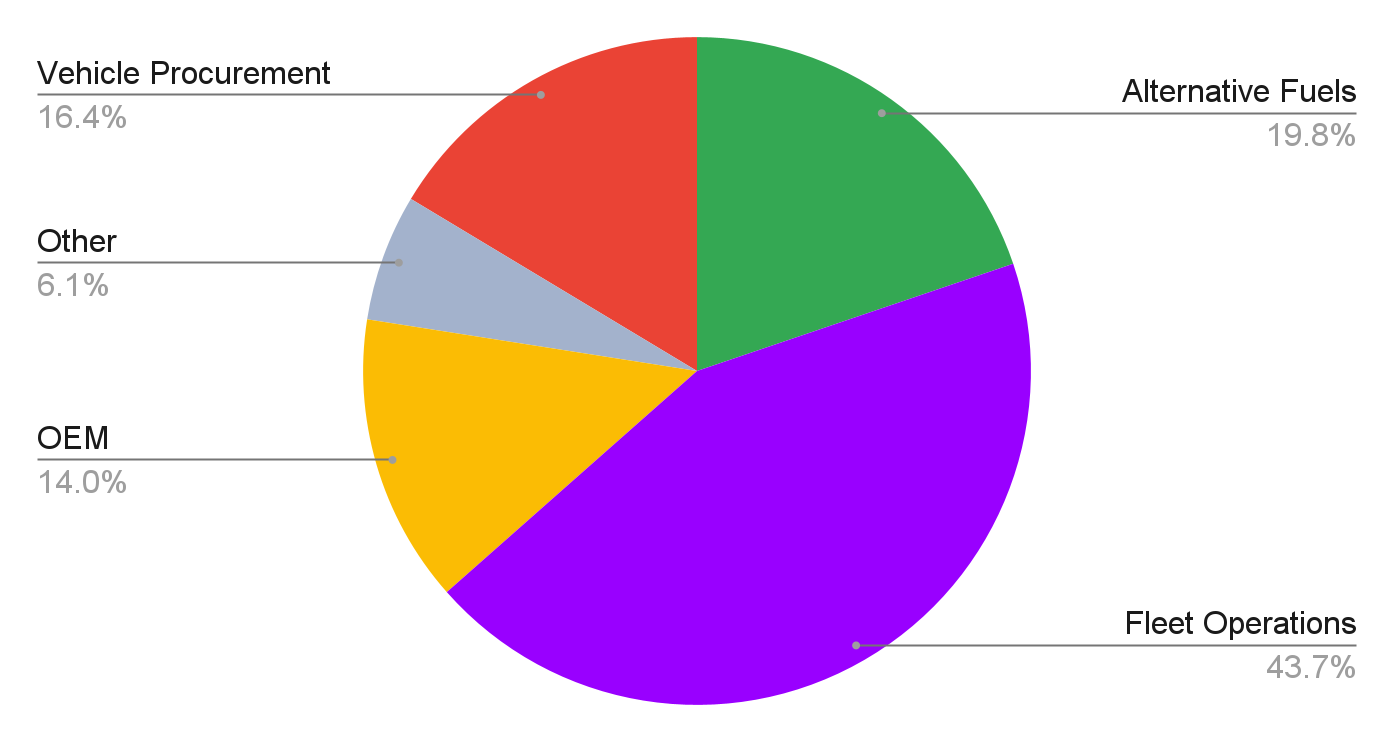

To do so, I mapped the 306 companies exhibiting at the event, divided into master categories (see chart) and into categories - for example, “Fleet Management Software” is under “Fleet Operations”.

Master categories of participants, % of total 306 companies exhibiting:

Let’s start with Alternative Fuels: most noticeable on the showroom floor were EV hardware and infrastructure solutions, with 54 presenters! 18.4% of total event presenters, almost 1 in 5, are geared to assist the industry to switch to electric. With so many solutions it's hard to differentiate; it seems that the “secret sauce” to obtain market leadership is focusing on a specific niche and/or having enough resources to create a great sales team and operational reputation. The Alternative Fuels category also comprises of a few EV retrofitting and Hydrogen solutions.

I had a chat with François Hoehlinger from TOLV, a EV retrofitting company who is working with Renault (and others) to allow fleets the ability to switch to electric while enabling companies to keep their (costly) interiors and extend current vehicles lifetime by up to 20 years. As for Hydrogen, I know Hydrogen makes sense with long-range trucks and buses (see Hydrogen ladder), but was a bit surprised to see Hysetco working with Toyota Mirai to advance the use of an everyday Hydrogen car.

There are many EV hardware / infrastructure players, battling to differentiate and offer a unique selling proposition. For now, the market is growing and there is still a blue ocean to go around.

Expect major consolidations starting to happen in a couple of years, when market growth stabilises and corporations & PEs start acquiring the more successful solutions. At 2nd place - with 41 presenters, 14% of total event presenters - were the OEMs. From Alfa Romeo to Volvo, they were all there. But nothing new or interesting, so let’s move on.

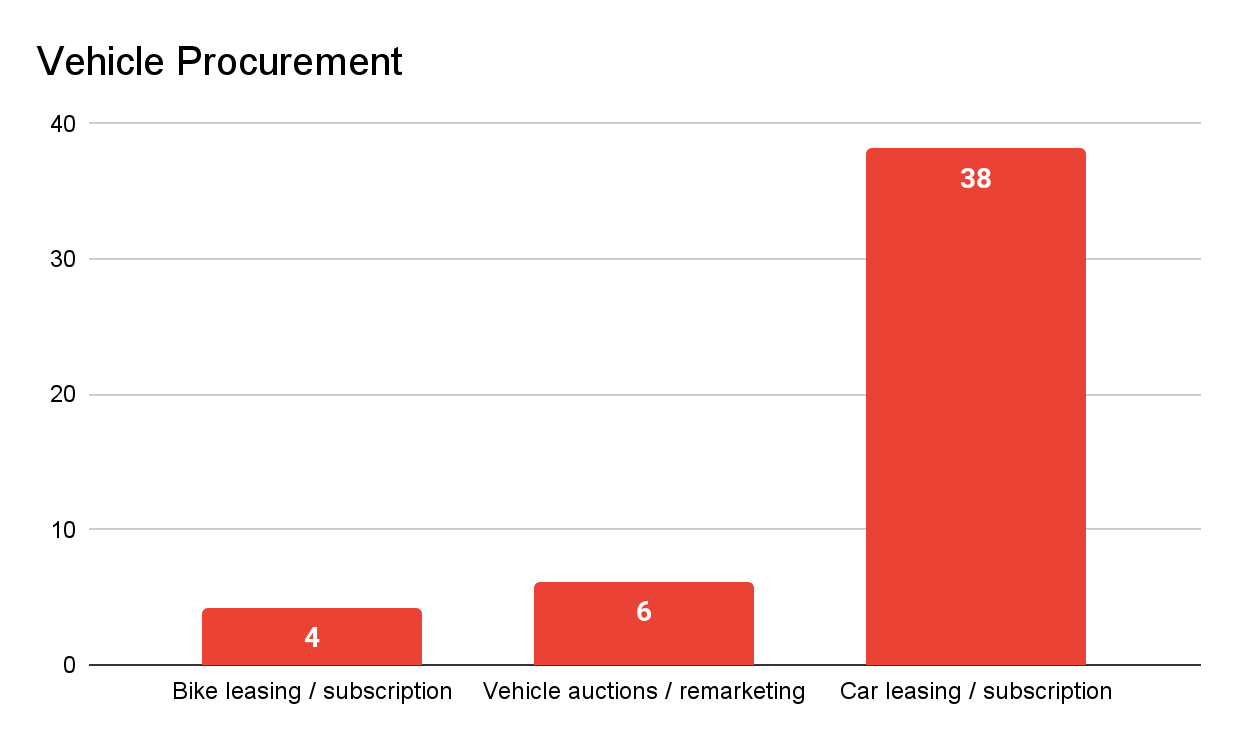

At 3rd place of total event presenters is car leasing/subscription solutions - a part of the Vehicle Procurement category. That category also hosts bike leasing/subscription and vehicle auctioneers / remarketers.

Number of presenters

Much like the EV infrastructure category, with so many players, differentiation is hard. I spoke to Olino Mobility, an all-EV premium B2B car-subscription player, who put the emphasis on the ability to be flexible and quicker than the big players. Pelikan Mobility focuses on business-critical fleets, offering a complete package which includes planning, infrastructure deployment and software to manage daily route optimisation. David Salfati stresses the benefits of Pelikan’s customised software - enabling fleets better ROI - as a differentiator.

Same as with EV hardware, so far market demand has been growing, enabling most companies to grow with it.

High interest rates and EV depreciation are key industry concerns. But with the market growing fast, demand for vehicles makes up for these challenges. I also spoke with Tandem and OOWI, which extend the bike offering to corporate fleets, mostly for commuting purposes but also for shared vehicles use cases. It works much like car subscription, in terms of time frame (up to 36 months) and coverage (insurance, maintenance etc.).

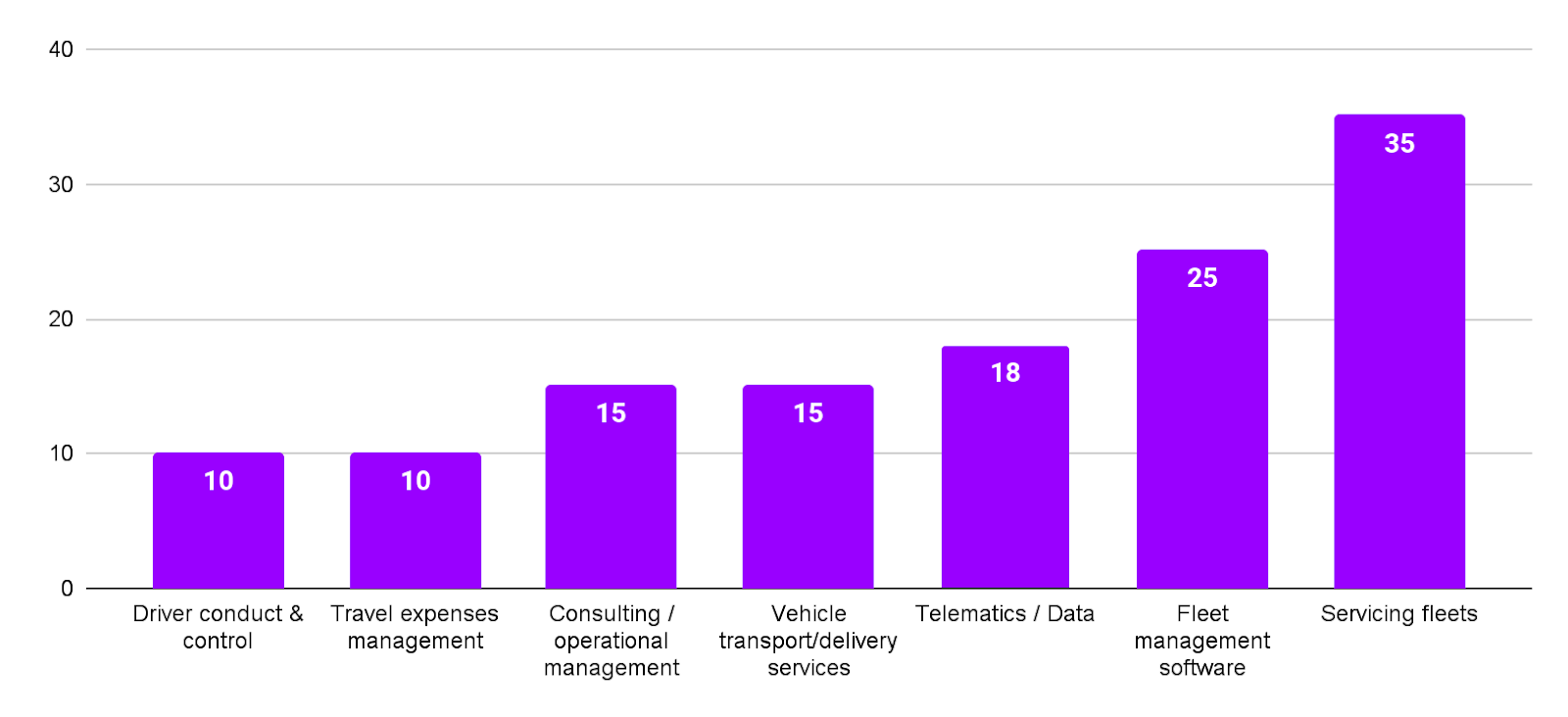

The Fleet Operations master category comprises 43.7% of total event presenters. I found interesting is that the very hands-on businesses, such as Fleet servicing (from tires to washing to work shops) and vehicle transportation/delivery services were very well represented, together comprising 17% of total event presenters.

The usual suspects are also all there - fleet management tools, telematic solutions, driver behaviour system - adding tools to the fleet manager’s belt.

To conclude:

Top of mind for fleets these days is the transition to EVs, the ability to procure the right vehicles and the ability to maintain those vehicles efficiently. the latter two have always been top of mind, with EV companies also becoming a familiar face.Methodology notes:

I mapped 293 of the 306 companies exhibiting; I took away duplicates, such as Mercedes exhibiting both cars and vans separately, or Stellantis offering financial services separately from the OEM booth.

Companies are often present in more than one category. I decided to allow each company only one representation, and chose the company’s main focus as its assigned category.

In the “Other” category are insurance, tax services, interior building, HR software and others.