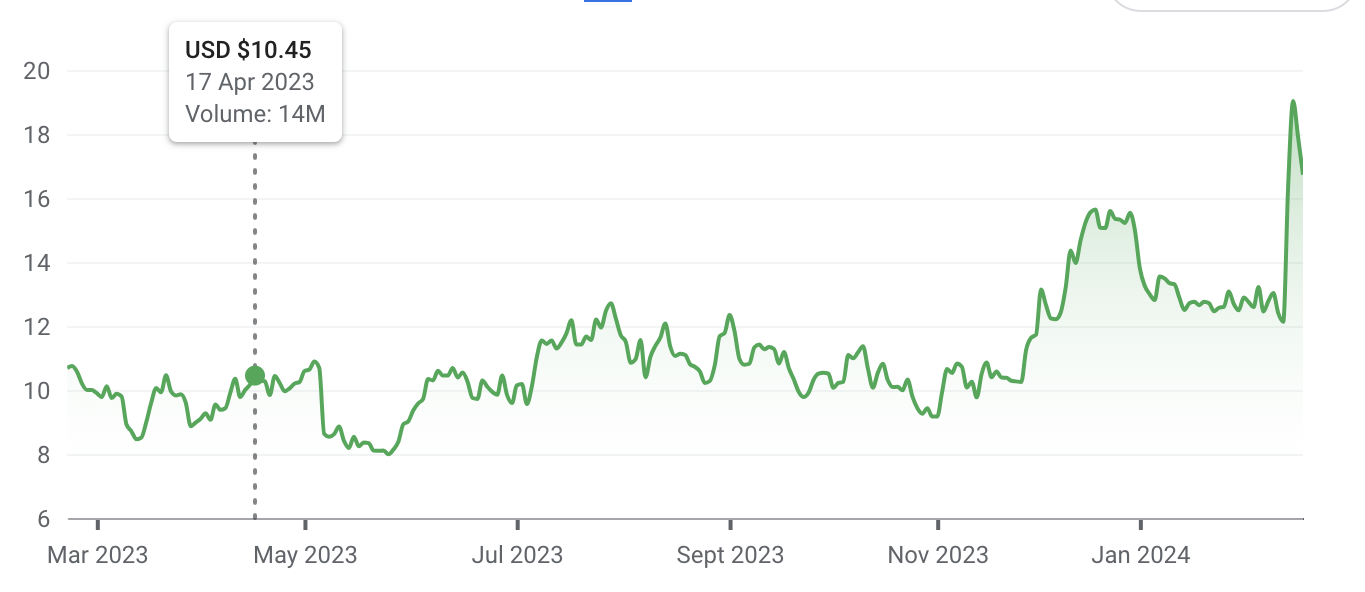

#movingpeople kicks off 2023 financial report season with Lyft - which has been under the leadership of David Risher since April 17th, 2023. During this time Risher has been able to (slowly) take the stock from ±$10 to ±$12, to (ignore the huge surge to the right of the stock chart, that originated from a typo in one of Lyft’s fillings) … to circa $16 today (Feb. 22nd).

Disclaimer: this is not financial advice. Do your own research, consult a professional, and be aware of potential risk.

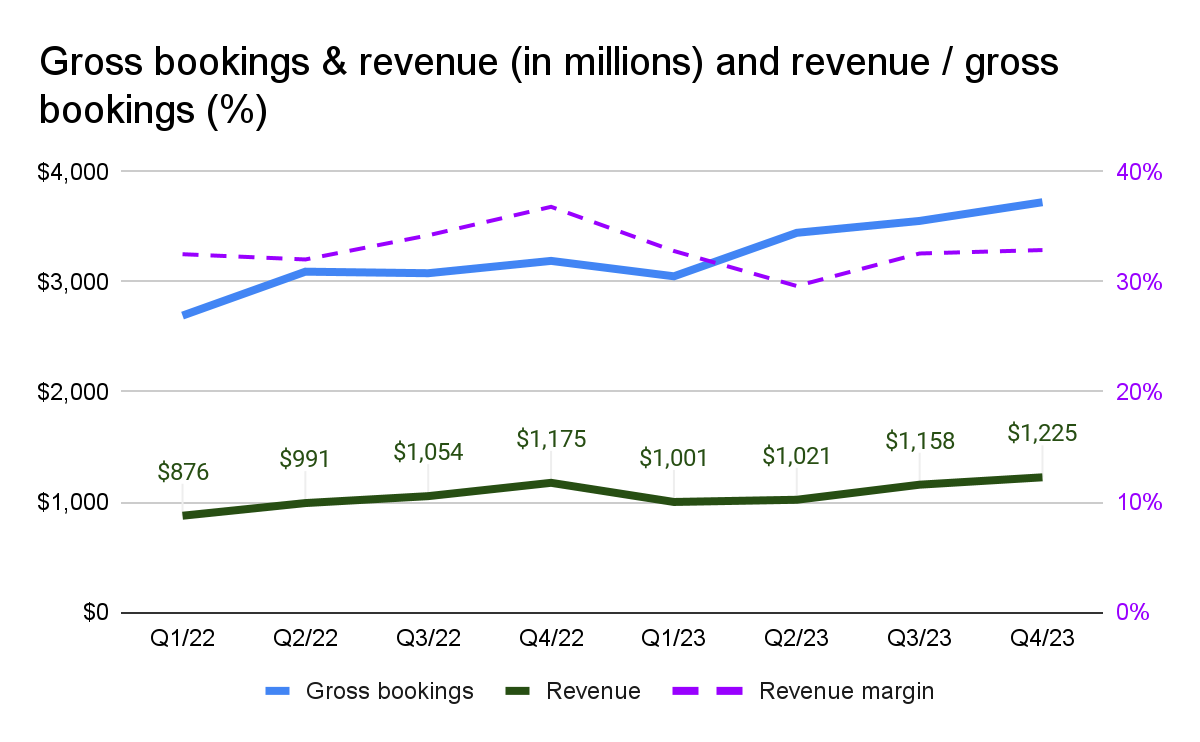

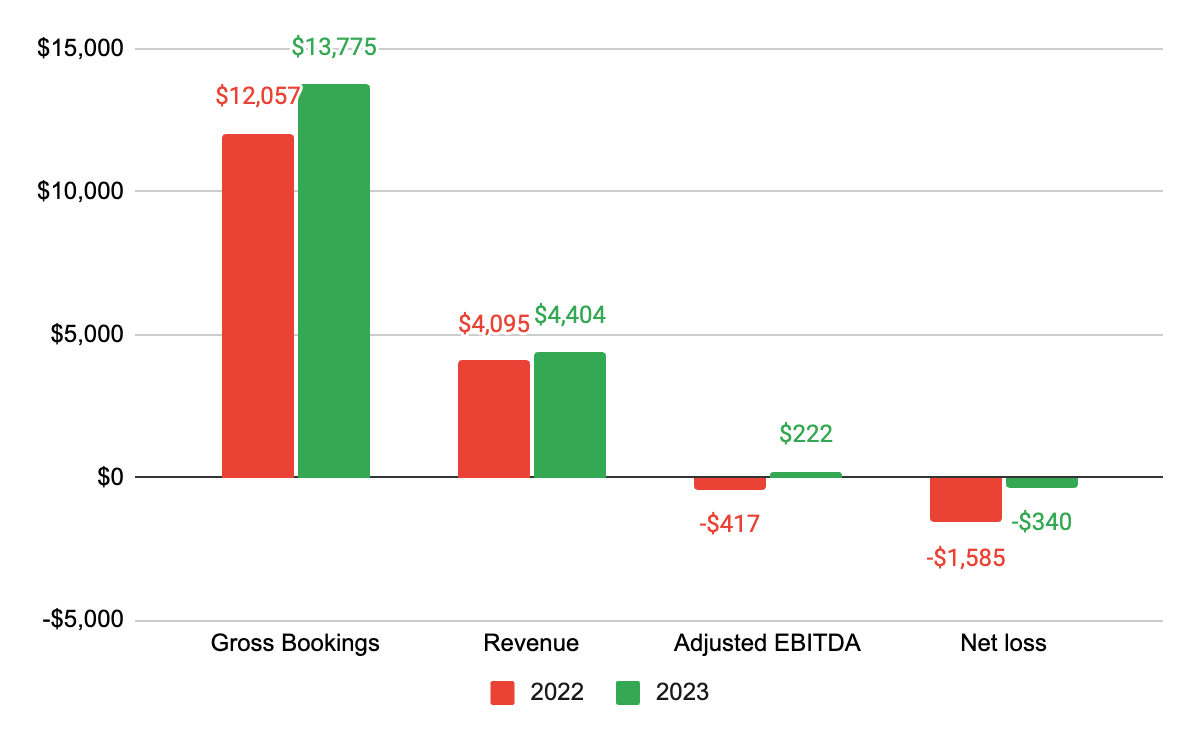

In 2023, Lyft is looking better across all fronts. Rides grew 18% YoY to 709 million; Gross Bookings grew 14% to $13.8 billion; Revenue grew 8% to $4.4 billion; and Adjusted-EBITDA is $222.4M, up from minus $416.5 in 2022.

Comparing 2022 to 2023, it is easy to see the improvement across key financial metrics:

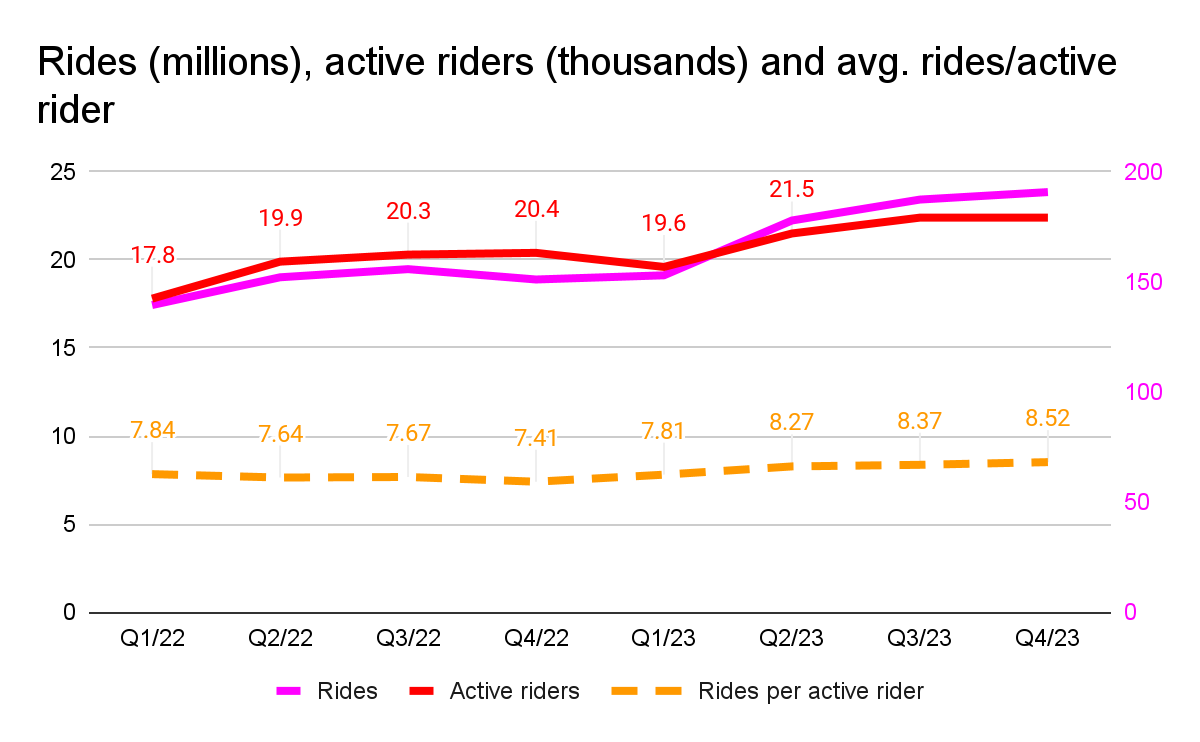

Below shows how things changed under Risher - since Q2/23 there have been more active riders taking more avg. rides, leading to a higher number of overall rides. Lyft was able to attract new drivers; in 2023, 25% of riders were new riders.

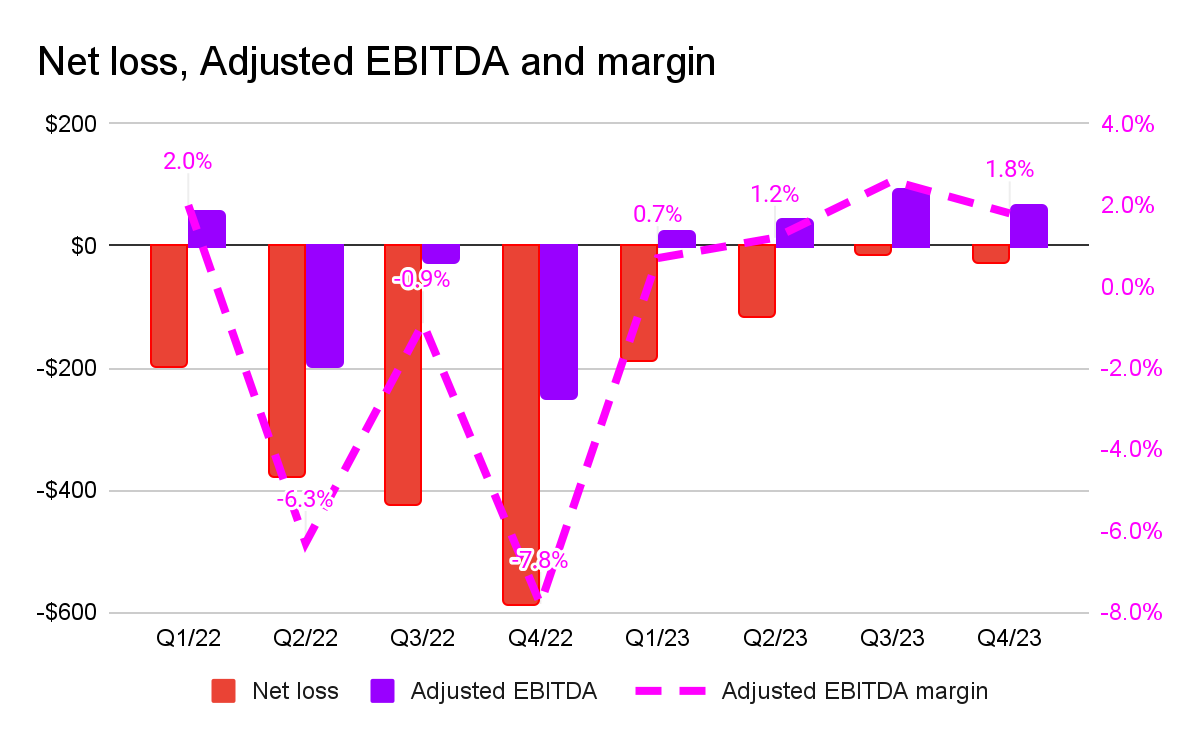

The next graph shows how Lyft’s losses shrink over time, with Adjusted-EBITDA and margin growing. Lyft’s Adjusted-EBITDA margin is defined as percentage of gross booking, and was 1.6% in 2023. There is still room for overall improvement - in FY23 Lyft’s loss amounted to $340.3M,

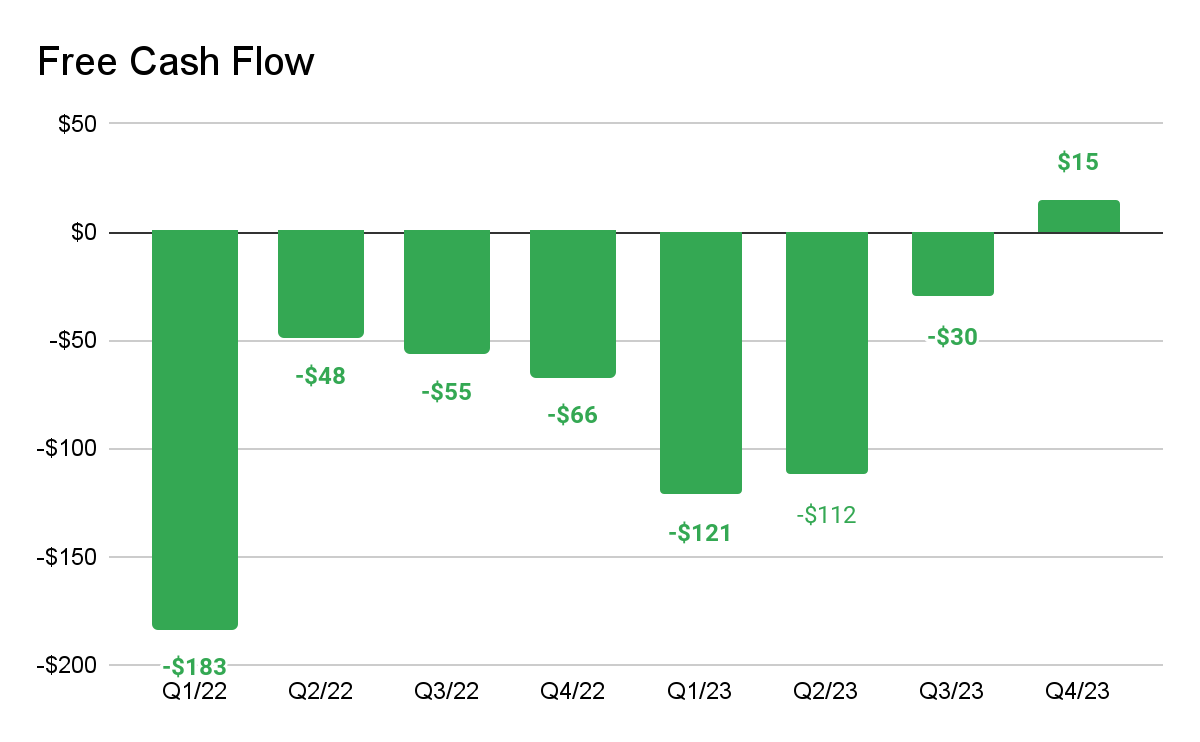

Lyft aims to be Free Cash Flow (FCF) positive in 2024, indicating its ability to sustain itself; in Q4/23, Lyft was able to generate positive FCF for the 1st time.

According to the company, Lyft will achieve positive FCF thanks to (1) better EBITDA margins; (2) reduced capital expenditure; and (3) general reduced cash outflows, for example switching to captive insurance. The expected FCF is half the 2024 adjusted EBITDA. I did the maths for you on that, expect circa $170M in FCF in 2024.

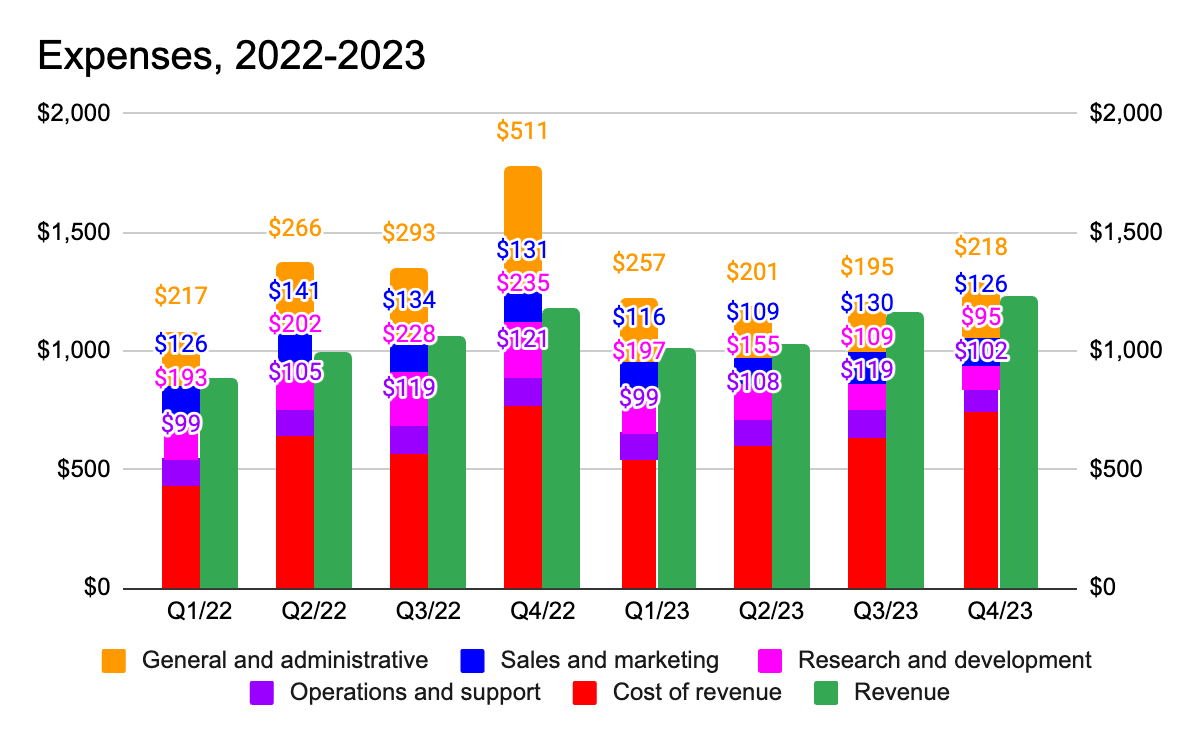

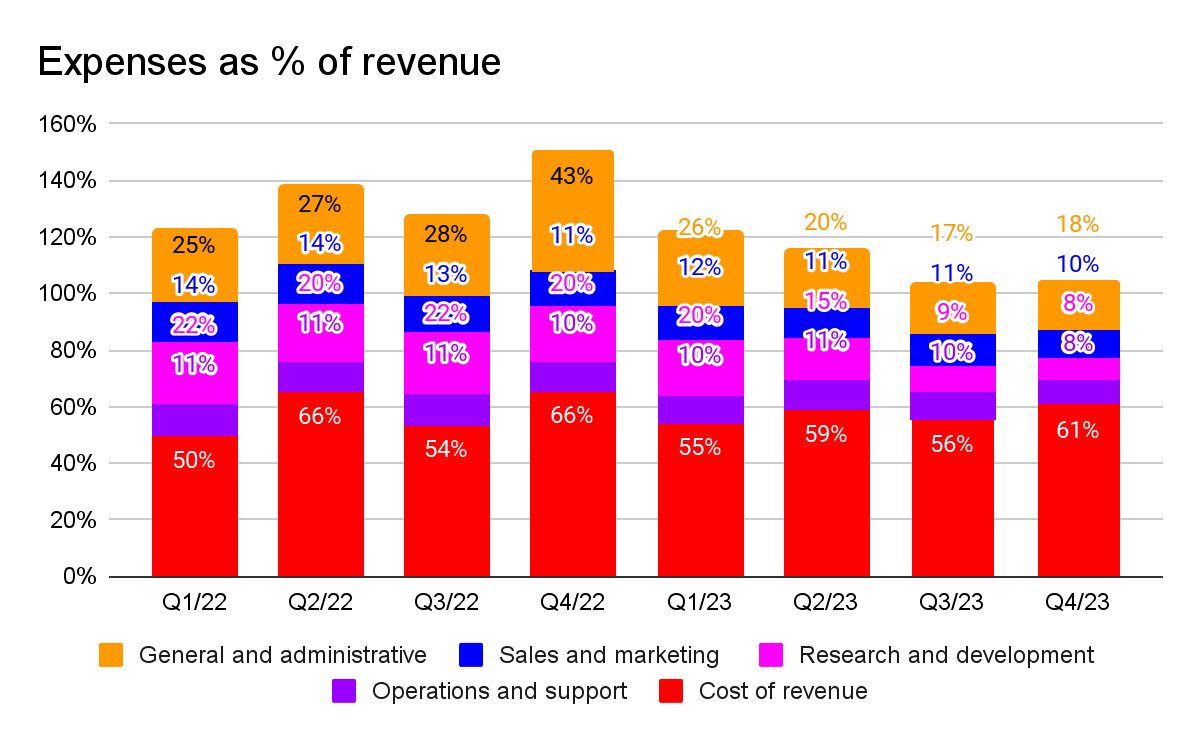

Reading through expenses, we can see that while cost of revenue stayed much the same (but less volatile), there have been cuts on G&A and on R&D and discipline on operations and S&M, which stayed at the same levels of expense despite revenue growing by 8%.

Looking ahead: 2024

Lyft focuses on three pillars of growth: (1) rider innovation, with programs such as women plus connect and improved airport rides experience; (2) driver attraction measures, such as with the latest commitment to guarantee drivers 70% of fare (excluding external fees); and (3) growth via B2B partnerships.

In 2024, Lyft expects to generate positive Free Cash Flow for the full year, by improving Adjusted EBITDA margin by 0.5% percentage points and by growing rides by mid teens and gross booking slightly faster.

My interpretation

Lyft has been on a growth trajectory since Risher took over, and the goal of achieving positive FCF in 2024 and profitability later on seem achievable. Lyft is focusing on its ride-hailing business, declaring it won’t go into delivery and trying to exit its bike business. the big question for Lyft will come in roughly 1.5 years - when profitability is achieved - and that question will be “what’s next”? Until then, the company will focus on operational and marketing excellence, so don’t expect any super-innovative moves from Lyft in the coming future.

Reading materials for those who wish to extra-deep-dive: